Russia’s invasion of Ukraine may have the unforeseen consequence of weakening the US dollar, and with it, reducing the United States’ heft in the global financial system.

The way this is happening is a strident effort by the Russian government to break economic ties with the United States and the European Union, and form new partnership with Eurasian countries and other powerful neighbors, including China and India.

Russia has proposed a gold and commodities-backed ruble, something we will get into shortly, as well as its own international standard of precious metals exchange dubbed the Moscow World Standard. According to Market Sanity,

With a new eastern-driven price discovery exchange, Russia believes it can break up the monopoly of the London Bullion Market Association (LBMA), which along with the CME Group’s NYMEX futures market, contains some of the world’s most influential gold, silver, platinum & palladium price discovery markets today.

In this article we explain how we got here, and what these new developments mean.

De-dollarization

The US dollar is the most important unit of account for international trade, the main medium of exchange for settling international transactions, and the store of value for central banks.

Lately though, “de-dollarization” is being pursued by countries with agendas at odds with the US, including Russia, China, Saudi Arabia and Iran.

Since 2018, the Bank of Russia has substantially reduced the share of dollars in its foreign exchange reserves, through purchases of gold, euros and yuan. As of March, 2022, Russia was the fourth largest holder of gold bullion, behind the US at no. 1, Germany, Italy and France. The country’s gold holdings have tripled since the first Russia-Ukraine war in 2014, and are estimated at around 20% of the BoR’s total reserves.

China and Russia have drastically reduced dollar usage in conducting trade. In 2015 about 90% of transactions used the dollar. After the trade war between the US and China broke out, the figure by 2019 had dropped to 51%. And that was before the war in Ukraine.

Bilateral currency swaps between Russia’s and China’s central banks helped Russia to bypass US sanctions in 2014. A three-year currency swap worth $24.5 billion, enabled each country to access the other’s currency without having to buy it on the foreign exchange market.

The Bank of Russia in early 2019 purchased $44 billion worth of Chinese yuan, tripling its share of Russia’s foreign exchange reserves from 5 to 15%. Russia’s yuan holdings are about 10 times the global average; it currently has nearly a third of all reserves in China’s renminbi/ yuan.

Major Russian energy companies including Gazprom and Rosneft have stopped using the US dollar, with the euro now the primary vehicle of trade between Russia and China. At the end of 2020 more than 83% of Russian exports to China were settled in euros. Although that too could be changing…

As the target of US economic sanctions (for annexing Crimea, interfering in its election, and now, invading Ukraine), Russia sees diversification from the dollar and into gold and other currencies, as a way of skirting trade restrictions.

Dollar competition

Yet according to the International Monetary Fund, as of the first quarter of 2022, 59% of global foreign exchange reserves were denominated in dollars, followed by the euro in second place at 20%.

This begs the question, if the US dollar were to be replaced, or made to compete with, another currency, what would it be? There is increasing evidence of a plan by the BRICS countries (Brazil, Russia, India, China, South Africa), to substitute the USD with a new global reserve currency.

At the 14th BRICS summit in June, Russian President Vladimir Putin said “The issue of creating an international reserve currency based on a basket of currencies of our countries is being worked out.”

He added that “contracts between Russian business circles and the business community of the BRICS countries have intensified…”

Experts say that a new global currency could either be an alternative to the IMF’s special drawing rights (SDRs), or be used only for settling trades between nations as opposed to a reserve currency used by central banks.

Recently it was reported that Russia and India no longer need the US dollar for mutual settlements, with the BRICS International Forum President telling reporters a new mechanism has been established between the two countries using only rubles and rupees.

Via Kitco, Purnima Anand also said a similar mechanism is being developed between Russia and China to eliminate the use of the greenback and employ only rubles and yuan.

This way of paying for goods gives Russia a way to go around the sanctions imposed on the country following its invasion of Ukraine.

“The BRICS countries are opening up to Russia, offering the opportunity for the country to overcome the consequences of sanctions,” Anand said.

Russia has also increased its ties with India, as trade jumped fivefold over the past four decades, according to Anand. India has been importing more oil from Russia, while Moscow has stepped up purchases of agricultural products, textiles, and medicine.

India has resisted the pressure from the West to ban Russian oil.

Gold and commodities-back ruble

In fact the Kremlin appears to have wasted little time, after approving what it calls the “special military operation” in Ukraine, in launching a project to pin the Russian ruble to gold and other commodities.

In an April interview with Russian newspaper Rossiyskaya Gazeta, one of the most powerful officials in Russia, Nikolai Patrushev said that,

For any national financial system to be sovereignized, its means of payment must have intrinsic value and price stability, without being pegged to the dollar.

Now experts are working on a project proposed by the scientific community to create a two-circuit monetary and financial system.

In particular, it is proposed to determine the value of the ruble, which should be backed by both gold and a group of goods that are currency values, and to put the ruble exchange rate in line with the real purchasing power parity.

Patrushev is no mere talking head. As Secretary of the Russian Federation’s Security Council, and a close Putin ally, his words should be seen as coming from the highest echelons of Russia’s government.

It is one of the clearest indications yet, that the Kremlin is actively working on creating a gold and commodity-backed ruble, with intrinsic value that is outside the orbit of the US dollar.

That Russia is distancing itself from its long-time Cold War adversary is unsurprising. More alarming is how Russia is attempting to build an alliance of countries, anchored by a common currency, or basket of currencies, in direct opposition to US economic hegemony.

The West vs The Rest

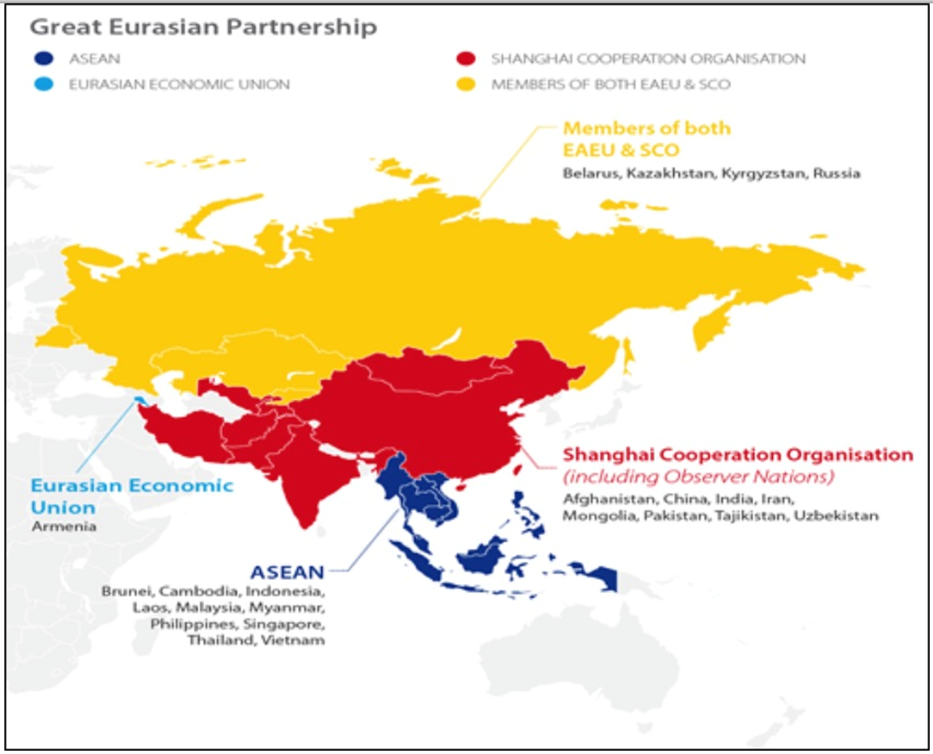

Patrushev alludes to “The West vs The Rest” concept in the above-mentioned interview. In it, he says Russia is moving from European to African, Asian and Latin American markets, giving priority to the EAEU, the BRICS and SCO countries.

The EAEU refers to the Eurasian Economic Union, comprised of Russia, Kazakhstan, Belarus, Armenia and Kyrgyzstan. BRICS is the acronym for Brazil, Russia, India, China and South Africa. SCO is a new (2021) grouping consisting of eight member states, China, Russia, India, Kazakhstan, Pakistan, Uzbekistan, Kyrgyzstan, and Tajikistan, as well as four observer states, Belarus, Iran, Afghanistan, and Mongolia, and a further six dialogue partners, Turkey, Azerbaijan, Armenia, Cambodia, Nepal and Sri Lanka.

Should the Western powers be concerned about these competing alliances? Well, according to Bullion Star columnist Ronan Manly, a conglomeration of 3 billion people using a gold and commodity-backed rouble is “Something for the Western media to ponder.” No kidding. (the West has also been forming new groupings to counter China and Russia, explained in our article on ‘Friend-shoring’)

Furthermore, Manly’s conclusion in late March when the Bank of Russia offered to buy gold from Russian banks at a fixed price of 5,000 rubles per gram, was that this was the first step in linking the ruble to gold. That move also put a floor price under the ruble and acted as a catalyst for the ruble to re-strengthen ground against the US dollar that had been lost in late February / early March.

During the same week in late March, Putin also informed the global market that non-friendly importers of Russian gas would have to pay for Russian natural gas using rubles. That move (which we are now seeing playing out in the EU) was the other side of the equation, linking the ruble to commodities…

What we are seeing now is Nikolai Patrushev and the Kremlin confirming this simple equation of linking the Russian ruble to gold and commodities. In other words, the beginning of a multilateral gold and commodity backed monetary system, i.e. Bretton Woods III.

In asking whether a new commodity-backed global reserve currency supported by China and Russia could become a reality, the Epoch Times notes that trade between Russia and the BRIC nations during the first quarter of 2022 increased 38% to $45 billion. Russia recently edged Saudi Arabia to become China’s biggest oil supplier. The Saudis and Iran have begun accepting Chinese yuan instead of dollars for their oil.

Moscow World Standard

Introduced at the top, the Moscow World Standard would have Eurasian Economic Union nations such as Russia, Belarus, Kazakhstan and Kyrgyzstan. It aims to add major gold and other precious metal trading nations like India, China, Peru, Venezuela, and other countries in South America and Africa where precious metals are mined.

The LBMA system has allowed PM values to be kept artificially low. Moscow understands that this is an unfair practice and negatively affects precious metals exporters. Russia and its partners account for about 57% of new physical gold supplies for the world each year, and with the inclusion of Venezuela and Peru, that stake would increase to 62%. (a little-known fact is that Russia’s biggest non-energy export is gold bullion, worth about $15 billion last year).

So here we have the majority of the world’s precious metals-producing nations, possibly setting up their own price discovery cartel, to take on the longstanding LBMA.

How would the MWS work in practice? According to press reports, it would be a specialized international brokerage headquartered in Moscow, with a price-fixing committee comprised of central banks from the EAEU including Russia, Kazakhstan, Belarus, Kyrgyzstan, and Armenia. Membership would also be available to large gold players such as China, India, Venezuela and Peru.

An article in Goldcore, via Dollar Collapse, notes the MWS’s formation was largely due to the LBMA in March suspending the accreditation of Russian precious metals refiners, followed by a ban imposed by G7 nations on Russian gold exports to the UK, Canada, the US and Japan. The European Union and Switzerland, a major gold refining hub, followed suit last month:

With LBMA at the heart of global precious metal trading being located in the UK, this shut Russia out of formal international markets for gold and silver.

So Russia sought alternative buyers. It didn’t have to look far.

The Moscow Times reported on Aug. 26 that Russia has significantly ramped up gold exports to China, with the latter importing $108.8B worth of Russian bullion in July. That’s a 750% increase from June and a whopping 4,800% increase from the same month last year.

According to the newspaper, market experts interviewed by RBC said they believe that Russia, the world’s second largest gold producer at more than 300 tons per year, is currently selling its metal to China at a discount of more than 30%. Others speculate that China is just one of several new destinations for Russian gold, in Asia and the Middle East.

Conclusion

To be sure, the United States will not easily give up the dollar’s role as both the reserve currency and as the monetary unit in which trade payments are settled. Wars have been fought over less and I expect that any serious threats to USD hegemony will be seriously resisted.

On the other hand, market forces might dramatically reduce the number of US dollars needed, especially given America’s waning influence in the Middle East and in Asia, where China’s regional power base is rapidly expanding. There is also the issue of the US national debt.

A country as highly leveraged as the United States risks defaulting on its debt, as Russia did in June, after Western sanctions shut down payment routes to overseas creditors.

The national debt currently sits at $30.8 trillion, with interest payments amounting to nearly $600 billion. Each interest rate rise means the federal government must spend more on interest. Higher debt servicing costs take away from other spending that that will have to be cut, as the government tries to keep its annual budget deficit under control.

The Congressional Budget Office has warned that US federal debt is expected to hit 185% of GDP within the next 30 years, which seems entirely possible, given the current debt to GDP ratio is 124%.

China and Russia have both indicated their disinterest in holding US Treasury debt, and have sold substantial amounts of their dollar-denominated holdings.

At the beginning of 2018, Russia held almost $100 billion worth of US Treasury bonds, but by early 2020, that figure had fallen to about $10 billion. As of April 2022, its Treasury holdings were just $2 billion.

If de-dollarization and a sell-off of US Treasuries were to happen on a larger scale than currently, the buck’s value would decline accordingly, paving the way for higher commodity prices including gold.

Source : Investor Ideas